Turn Your Vancouver Home Equity Into Cash Without Selling (2026)

Your Home Has More Value Than You Think

You have been making mortgage payments for years. Maybe a decade. Maybe longer. And somewhere along the way, Vancouver real estate did what it always does: your property went up in value.

So here you are. You own a home worth well over a million dollars, but you still have a mortgage, and there is a significant gap between what the property is worth and what you owe. That gap is your equity. And the question most people quietly wonder but never ask is: can I actually use it?

The answer is yes. You do not have to sell the house to access the value inside it. Here is how it works.

What You Are Actually Sitting On

The benchmark price of a home in Metro Vancouver was $1,100,700 in May 2026. If you bought five or more years ago, there is a strong chance you are sitting on significant equity, even after the correction from the 2022 peak.

Home equity is simply the difference between what your property is worth today and what you still owe on your mortgage. That is the number lenders look at when you want to borrow against it. And in most cases, you can access up to 80 percent of your home's appraised value across all debts combined.

That means if your home is worth $1,100,000 and you owe $480,000 on your mortgage, you could potentially access up to $400,000 in additional borrowing. What you use it for is your business.

"Most Vancouver homeowners have no idea how much borrowing power they are sitting on. The bank is not going to bring it up unprompted."

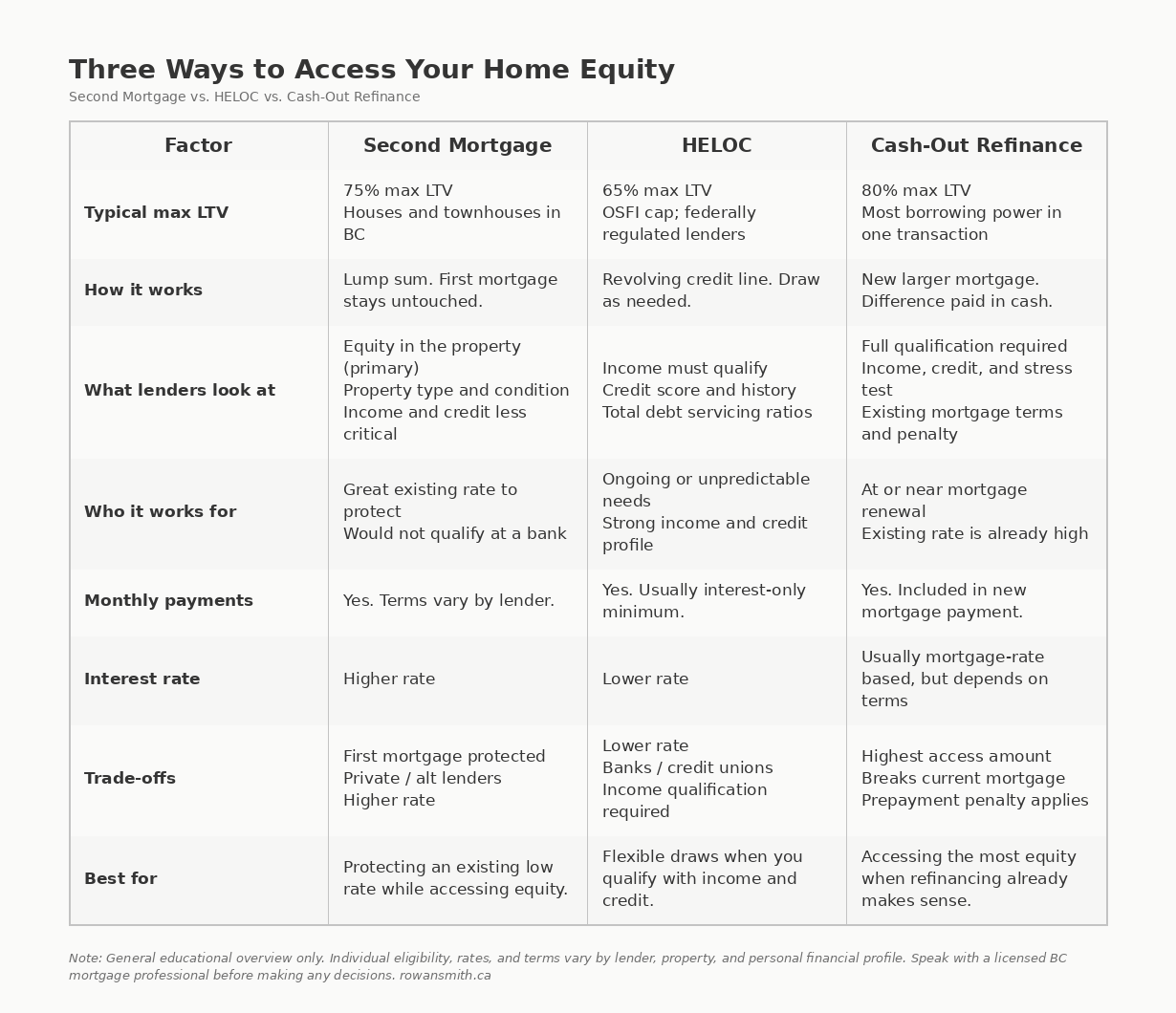

The Three Ways to Access It

A Second Mortgage

A second mortgage is a separate loan registered behind your existing first mortgage. Your first mortgage stays completely untouched. You receive a lump sum and make fixed payments on the second loan only.

This is the most common option for people who locked in a great rate on their first mortgage and have no interest in breaking it. You keep the rate you have and access the equity sitting on top of it.

Private and alternative lenders in BC can lend up to 75 percent of your home's value on a second mortgage for houses and townhouses. They focus primarily on the equity in the property, not on your income or your credit score. That opens the door for homeowners who would not qualify at a bank.

A HELOC

A HELOC is a Home Equity Line of Credit. Think of it like a credit card that is secured against your property. You get approved for a limit and draw from it as you need, paying interest only on what you actually use.

Canada's prime rate is currently 4.45 percent as of June 2026, held steady by the Bank of Canada for five consecutive announcements. Most HELOCs are priced at prime plus a small margin, which puts them in the 4.95% to 5.50% range for well-qualified borrowers through a traditional lender.

Federally regulated lenders are capped at 65 percent loan-to-value for a standalone HELOC under OSFI rules. So if your goal is maximum flexibility rather than maximum access, this is the product for that.

A Cash Out Refinance

A refinance replaces your entire mortgage with a new, larger one. You get the difference in cash at closing. This gives you the most borrowing power in one transaction, but it means breaking your current mortgage, which triggers a prepayment penalty.

On a large Vancouver mortgage, that penalty can be significant. This option makes the most sense at renewal time, or when your existing rate is already high, and refinancing saves you money regardless of the penalty.

Who Is This For

This is not just for people with perfect credit and a T4. Equity lending works across a much wider range of situations than most people realize.

You might be self-employed, and your income on paper does not reflect what you actually earn. You might have bruised credit from a few years ago, but you have been paying your mortgage on time. You might be going through a life change and need access to capital quickly. You might simply want to consolidate high-interest debt, fund a renovation, cover a business gap, or use your equity as a down payment on an investment property.

The common thread across all of these is that you own a home in a strong market, and there is real value sitting in it. That is what matters most to an equity lender.

"The bank looks at you first and the property second. Equity lenders look at the property first. That is a fundamental difference, and it changes who qualifies."

What It Costs and What to Watch For

Equity lending costs more than your primary mortgage. That is the truth, and it is worth understanding before you proceed.

Private second mortgage rates in BC currently run from around 8 to 14 percent depending on the lender, the property, and how much equity is in the deal. On top of the interest rate, you will have lender fees, a required appraisal, and legal costs for a BC notary or lawyer to register the new mortgage.

The goal is always to use equity lending as a bridge. You solve the immediate problem, and you have a clear plan for what comes next, whether that is rebuilding your credit, stabilizing your income, or refinancing back into conventional terms when the timing is right.

One thing to know before you apply: if you have CRA tax arrears or if a CRA lien has been registered against the property, that CAN sit ahead of most lenders and needs to be resolved first, especially if it is a GST arrears. This comes up more often than people expect, and sometimes borrowers are not aware of it until a title search is done.

What Lenders Actually Look At

If you are working with a private or alternative lender, they are not running your application through a bank's automated scorecard. Here is what they focus on.

- Loan-to-value ratio: The lower that number, the more comfortable the lender. A deal at 60 percent loan-to-value is a very different conversation from one sitting at 78 percent.

- The property itself: Location, condition, and type all matter. A well-located Vancouver detached home is a different risk profile from a rural property or a strata unit with stale financials.

- Your exit strategy: Private mortgages are typically one to two years. The lender wants to know what changes in that window. How do you refinance, sell, or pay this down at maturity? A clear, realistic answer to that question is often the difference between an approval and a decline.

The Conversation Worth Having

Most homeowners in Greater Vancouver have more options than they realize. The challenge is that no one walks you through them unless you ask.

Your bank will tell you what you qualify for at their institution. Rowan can show you what is available across the full market, from traditional lenders to alternative lenders to private capital, and help you figure out which product actually fits your situation and your timeline.

Sometimes the best move is to access equity right now. Sometimes the best move is to wait six months and approach it differently. The only way to know is to look at your actual numbers with someone who knows all the options.

Ready to find out what your Vancouver home equity can do for you? Contact Rowan for a free, no-obligation conversation. Bring your questions, and he will walk you through your possibilities.