Reverse Mortgage, HELOC, or Downsizing? A BC Homeowner's Guide to Accessing Equity After 55

Owning a Home in BC Changes Everything for You, and Here is Why

If you own a home in Greater Vancouver and you're over 55, you're likely sitting on significant equity. Decades of rising property values across Metro Vancouver (Burnaby, Richmond, North Vancouver, Surrey, and beyond) have made long-time homeowners equity-rich in a way that's genuinely rare globally.

Right now, more BC homeowners than ever are asking whether to tap their home equity and, if so, which option makes the most sense.

Three options come up most often: a reverse mortgage, a home equity line of credit (HELOC), or selling the home and downsizing. Each works differently, costs differently, and fits a different kind of situation. None of them is automatically the right answer.

This guide breaks down all three, in plain English, so you can understand your options before you talk to anyone.

Why BC Homeowners Over 55 Are Asking This Question

Retirement in Canada looks different from what it did a generation ago. Defined benefit pensions are less common. The cost of living, especially in the Lower Mainland, has climbed faster than most people planned for. And many homeowners find themselves in a position that sounds straightforward but feels complicated: a lot of their net worth is locked inside the walls of their home.

Some of the real situations I hear from clients include:

- A pension that covers the basics, but not travel, home care, or helping adult children with a down payment

- A home that needs significant repairs or modifications for aging-in-place, but not enough cash flow to fund the work

- A desire to stay in a long-time home in a neighbourhood they love, without wanting to draw down RRSPs early and trigger a large tax hit

- Adult children struggling to get into the Vancouver housing market, with parents who want to help but don't want to sell

These are real situations, not hypotheticals. And they're why the conversation around home equity access has grown so much in BC over the past few years.

What Is a Reverse Mortgage? (The Short Version)

A reverse mortgage lets homeowners aged 55 and older borrow against their home equity without making monthly mortgage payments. The loan becomes due only when you sell the home, move out permanently, or pass away. At that point, the proceeds from the home sale are used to repay the loan balance, including accumulated interest.

The key features, confirmed by the Financial Consumer Agency of Canada (FCAC):

- Age: All owners on title must be 55 or older.

- Primary residence only: You must live in the home for at least six months of the year.

- Maximum borrowing: Up to 55% of the appraised value of your home. How much you actually qualify for depends on your age, your property's location, and its type and condition.

- No monthly payments required: You are not required to make any payments while you live in the home.

- Tax-free funds: The money you receive does not count as income. It does not affect Old Age Security (OAS) or the Guaranteed Income Supplement (GIS).

- You keep ownership: The home stays in your name. A common misconception is that the bank takes possession. It does not.

- Interest compounds over time: Because no payments are made, interest is added to the loan balance. The longer the loan runs, the more is owed.

- Important: Reverse mortgage interest rates are higher than standard mortgage rates. The total amount owed can grow significantly over time. A $400,000 reverse mortgage at a hypothetical 7% annual compounding could grow to approximately $786,000 after 10 years, and over $1.5 million after 20 years.

These are illustrative numbers only. Actual rates vary by lender and are subject to change. Request a personalized illustration before making any decisions.

In British Columbia, the main reverse mortgage providers are HomeEquity Bank (which offers the CHIP Reverse Mortgage), Equitable Bank, and Bloom Financial. Access through a broker varies by lender. I can help you understand which products are available in your specific situation.

What Is a HELOC and Who Can Use One?

A home equity line of credit (HELOC) is a revolving credit facility secured against your home. You borrow what you need, when you need it, up to your approved limit. You only pay interest on what you've actually drawn, not the full credit limit.

Under federal mortgage rules (the B-20 guideline), lenders can offer HELOCs up to 65% of your home's appraised value, subject to your total outstanding mortgage not exceeding 80% of the home's value.

The critical difference from a reverse mortgage: you must qualify. That means demonstrating sufficient income and a strong credit profile. For retirees living primarily on a fixed pension, CPP, and OAS without employment income, qualifying for a HELOC can be challenging, depending on the lender and the overall picture.

If you can qualify, a HELOC typically offers:

- Lower interest rates:

Usually lower than reverse mortgage rates, often tied to the prime rate.

- Flexibility:

Borrow and repay as needed. You're not committed to a lump sum.

- Interest-only minimum payments:

You are typically required to make at least interest payments on what you've drawn.

- No age restriction: Available to homeowners of any age who qualify financially.

For homeowners who can qualify (for example, if you have rental income, a strong pension, or investment income), a HELOC is often the more cost-effective choice. The trade-off is the income and credit requirement, and the fact that monthly payments are required.

What Does Downsizing Actually Look Like in the Lower Mainland?

Downsizing, which means selling your current home and purchasing or renting something smaller, is often the first idea people have. And in many parts of Canada, it genuinely frees up a significant amount of capital.

In Greater Vancouver, the picture is more complicated.

The gap between a detached home and a smaller alternative (a condo, townhouse, or rental) is narrower here than almost anywhere else in Canada. Depending on the neighbourhood, downsizing from a detached home to a two-bedroom condo might free up some capital, but often less than people expect, particularly after accounting for:

- Real estate commissions

- Legal fees and disbursements on both the sale and the purchase

- Moving costs and any renovation required on the new property

- Potential property transfer tax on the new purchase

- Strata fees, which are a new ongoing cost for many condo purchasers

For some homeowners, downsizing also carries a non-financial cost: leaving a neighbourhood they've lived in for 30 years, moving away from friends, community connections, and familiar routines. That's a real consideration, and it matters.

That said, downsizing may make the most financial sense in specific situations, particularly if you plan to rent rather than buy, or if you're moving to a lower-cost area.

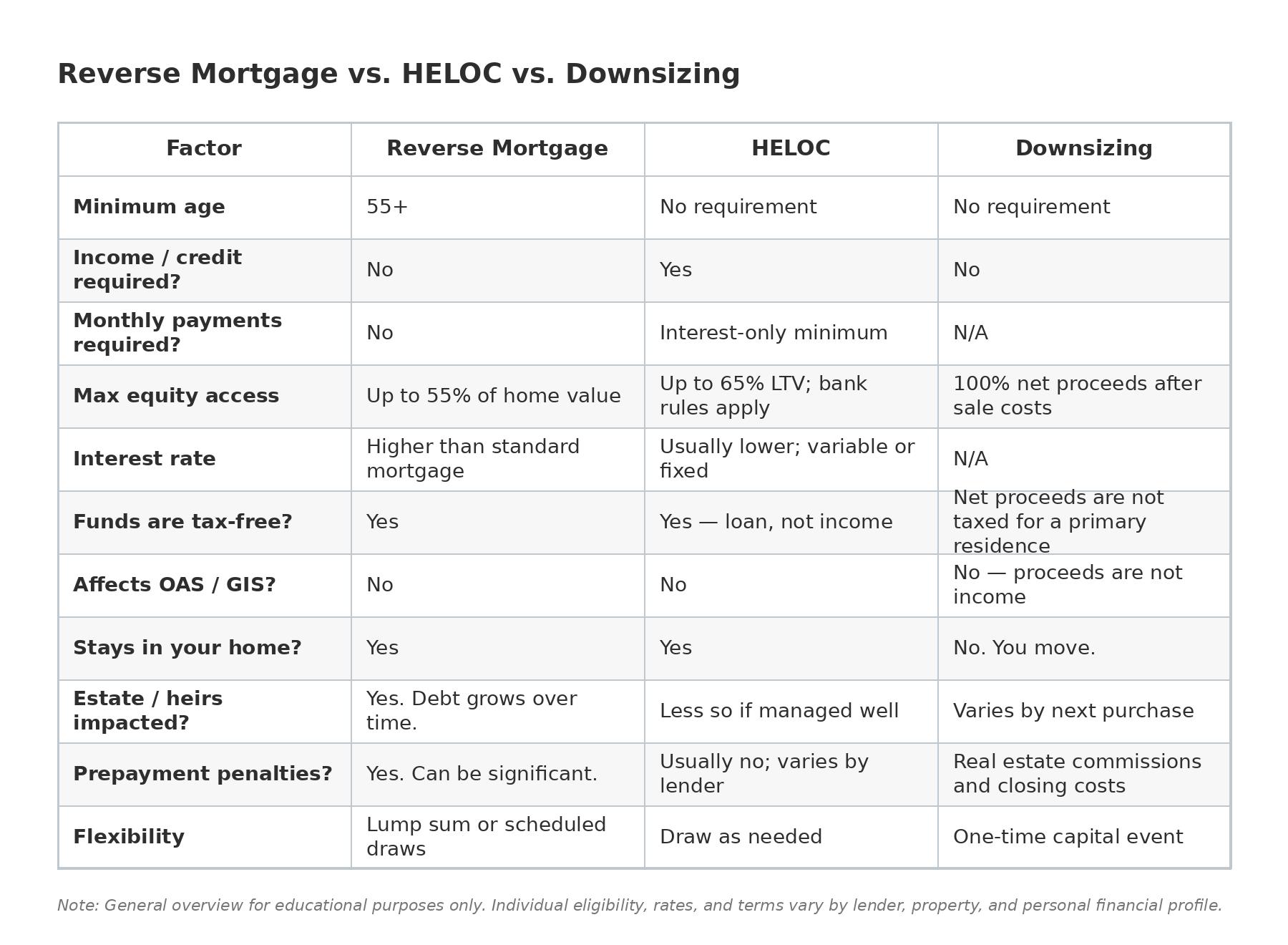

Side-by-Side Comparison

Here's a summary of how these three options compare across the factors that matter most:

When a Reverse Mortgage Might Make Sense

A reverse mortgage is not the right product for everyone, but it is genuinely the right fit for some homeowners. It tends to make the most sense when:

- You have little to no qualifying income, making a HELOC difficult or impossible to obtain

- You want to stay in your home long-term and have no intention of selling within the next several years

- You need tax-free funds and are concerned about the impact on government benefits like OAS or GIS

- You need cash for home care, home modifications, medical expenses, or to supplement a fixed income

- Your heirs are aware of the arrangement and are not relying on inheriting the home's full equity

- You want access to funds without taking on monthly payment obligations

The longer you intend to stay in the home and the older you are when you take the reverse mortgage, the less impact the compounding interest will have over your expected timeline. Age matters significantly in reverse mortgage planning.

When a Reverse Mortgage Might Not Be the Best Fit

There are situations where a reverse mortgage is not the best tool. A good broker should tell you that honestly:

- You're planning to sell or move within a few years, since prepayment penalties on reverse mortgages can be significant

- You can qualify for a HELOC, which may give you lower-cost access to the same funds

- Your heirs have a strong expectation of inheriting the home's full equity, and reducing that equity meaningfully affects their plans.

- Your property type (certain condos, manufactured homes, or rural properties) may not qualify or may receive a lower valuation.

- A refinance or second mortgage might be a more cost-effective solution for your specific situation.

The goal of any conversation I have with a client about reverse mortgages is to make sure it actually fits their situation, not just to arrange one because they asked about it.

One Thing to Understand About Timing

If you're considering a reverse mortgage, timing is worth understanding, though not in the way it's often framed.

Because interest compounds on a reverse mortgage (no payments are made, so the balance grows), the earlier you take one, the longer interest has to accumulate. A reverse mortgage taken at 60 will result in a significantly larger debt load by age 75 than one taken at 70, all else being equal.

This doesn't mean you should rush. It means the decision benefits from a clear-eyed look at how long you plan to stay in the home, what you need the funds for, and whether an alternative option might serve you better in the short term while preserving more flexibility.

A proper plan is more valuable than a fast decision.

How a Mortgage Broker Fits Into This Decision

A licensed mortgage broker's role, at least the way Rowan approaches it, is to help you understand all the options before choosing one.

That means comparing reverse mortgage products across providers, exploring whether a HELOC is feasible given your income and credit profile, running the numbers on refinancing alternatives, and being upfront when none of the mortgage-based options is actually the best move.

The reverse mortgage market in BC is growing quickly. Over $8.2 billion in reverse mortgage debt was outstanding in Canada as of mid-2024, up more than 18% year over year, according to industry data. That growth reflects real demand from homeowners who need income solutions. It also means there are more salespeople in this space than ever. Making sure you're talking to someone with access to multiple providers, not just one, matters.

Frequently Asked Questions

What is the minimum age for a reverse mortgage in Canada?

All owners listed on the title must be at least 55 years old. If you have a spouse or co-owner who is under 55, that affects eligibility. This is worth confirming with a broker before applying.

Does a reverse mortgage affect my OAS or GIS payments?

No. Funds received from a reverse mortgage are loan proceeds, not income. They do not count toward your net income for OAS recovery (the clawback) or GIS eligibility. This is confirmed by the Financial Consumer Agency of Canada. That said, if you invest the proceeds and earn returns, those returns may affect your income picture. Speaking with a financial planner is recommended if this is relevant to your situation.

Is the money from a reverse mortgage taxable in Canada?

No. The funds are a loan, not income, and are received tax-free. However, tax implications can arise depending on how you use the funds. Consulting a tax professional for your specific situation is always recommended.

Can I get a reverse mortgage on a condo in Vancouver?

In many cases, yes, but it depends on the building. Condo type, strata corporation health, and property condition can all affect eligibility and valuation. Rowan can help you understand whether your specific property qualifies.

What happens if I outlive my reverse mortgage?

You cannot 'run out' of a reverse mortgage in the traditional sense. You remain in your home until you choose to sell, move out permanently, or pass away. There is no point at which the lender forces you out while you continue to live in and maintain the property and meet the basic loan conditions (such as paying property taxes and maintaining the home). Canadian regulations protect borrowers in this regard.

Can I pay off a reverse mortgage early?

Yes. You can repay a reverse mortgage at any time. However, prepayment penalties typically apply, and they can be significant depending on how early you repay and which lender you used. This is one reason to think carefully before taking a reverse mortgage if you expect to sell within a few years.

What fees are involved in setting up a reverse mortgage in BC?

Setup costs typically include an independent legal advice fee (required), a home appraisal fee, and potentially an administration or origination fee, similar in structure to closing costs on a standard mortgage. These costs can often be rolled into the loan rather than paid upfront. Rowan can walk you through a full cost illustration before you commit to anything.

Who are the reverse mortgage providers in British Columbia?

The main providers currently operating in BC are HomeEquity Bank (the CHIP Reverse Mortgage), Equitable Bank, and Bloom Financial. Products, rates, and broker access vary by lender. Rowan can help determine which providers and products are accessible for your specific situation.

Ready to Understand Your Options?

Deciding between a reverse mortgage, a HELOC, and downsizing comes down to your specific situation: your age, your home value, your income, and what you want retirement to look like.

I help BC homeowners over 55 understand all three options clearly before making any decisions. Call Rowan and have a free consultation.